UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE

SECURITIES EXCHANGE ACT OF 1934

For the

fiscal year ended December 31, 2017

Commission

File Number: 000-08092

GT BIOPHARMA, INC.

(Exact

name of Registrant as specified in its charter)

|

Delaware

|

|

94-1620407

|

|

(State

of incorporation or organization)

|

|

(I.R.S.

Employer Identification No.)

|

1825 K

Street NW, Suite 510

Washington, DC 20006

(Address

of principal executive offices) (Zip code)

(800) 304-9888

(Registrant’s

telephone number including area code)

Securities

registered pursuant to Section 12(b) of the Act: None.

Securities

registered pursuant to section 12(g) of the Act:

|

Title

of Securities

|

|

Exchanges

on which Registered

|

|

Common

Stock, $.001 Par Value

|

|

None

|

Indicate

by check mark if the registrant is a well-known seasoned issuer, as

defined in Rule 405 of the Securities Act. Yes ☐ No

☒

Indicate

by check mark if the registrant is not required to file reports

pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No

☒

Indicate

by check mark whether the registrant (1) has filed all reports

required to be filed by Section 13 or 15(d) of the Securities

Exchange Act of 1934 during the preceding 12 months (or for such

shorter period that the registrant was required to file such

reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes ☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically

and posted on its corporate website, if any, every Interactive Data

File required to be submitted and posted pursuant to Rule 405 of

Regulation S-T during the preceding 12 months (or for such shorter

period that the registrant was required to submit and post such

files). Yes ☐ No ☒

Indicate

by check mark if disclosure of delinquent filers pursuant to Item

405 of Regulation S-K (§229.405) is not contained herein, and

will not be contained, to the best of registrant’s knowledge,

in definitive proxy or information statements incorporated by

reference in Part III of this Form 10-K or any amendment to this

Form 10-K. Yes

☐ No

☒

Indicate

by check mark whether the registrant is a large accelerated filer,

an accelerated filer, a non-accelerated filer, a smaller reporting

company, or emerging growth company. See the definitions of

“large accelerated filer,” “accelerated

filer,” “smaller reporting company,” and

“emerging growth company” in Rule 12b-2 of the Exchange

Act.

|

Large

accelerated filer☐

|

Accelerated

filer ☐

|

|

Non-accelerated

filer ☐ (Do not check if a smaller reporting

company)

|

Smaller

reporting company ☒

|

|

|

Emerging

Growth Company ☐

|

If an

emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided

pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined

in Rule 12b-2 of the Exchange Act). Yes ☐ No

☒

The

aggregate market value of the registrant’s common stock,

$0.001 par value per share, held by non-affiliates on June 30, 2017

was approximately $2.5 million. As of February 28, 2018, there were

50,117,978 shares of the registrant’s common stock, $0.001

par value, issued and outstanding.

Table

of Contents

|

PART

I

|

|

|

|

1

|

|

Item

1.

|

|

Business

|

|

1

|

|

Item

1A.

|

|

Risk

Factors

|

|

26

|

|

Item

1B.

|

|

Unresolved

Staff Comments

|

|

48

|

|

Item

2.

|

|

Properties

|

|

48

|

|

Item

3.

|

|

Legal

Proceedings

|

|

48

|

|

Item

4.

|

|

Mine

Safety Disclosures

|

|

48

|

|

|

|

|

|

|

|

PART

II

|

|

|

|

49

|

|

Item

5.

|

|

Market

for Registrant’s Common Equity, Related Stockholder Matters

and Issuer Purchases of Equity Securities

|

|

49

|

|

Item

6.

|

|

Selected

Financial Data

|

|

50

|

|

Item

7.

|

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

|

50

|

|

Item

7A.

|

|

Quantitative

and Qualitative Disclosures About Market Risk

|

|

56

|

|

Item

8.

|

|

Financial

Statements and Supplementary Data

|

|

56

|

|

Item

9.

|

|

Changes

in and Disagreements With Accountants on Accounting and Financial

Disclosure

|

|

56

|

|

Item

9A.

|

|

Controls

and Procedures

|

|

56

|

|

Item

9B.

|

|

Other

Information

|

|

57

|

|

|

|

|

|

|

|

PART

III

|

|

|

|

58

|

|

Item

10.

|

|

Directors,

Executive Officers and Corporate Governance

|

|

58

|

|

Item

11.

|

|

Executive

Compensation

|

|

59

|

|

Item

12.

|

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters

|

|

62

|

|

Item

13.

|

|

Certain

Relationships and Related Transactions, and Director

Independence

|

|

64

|

|

Item

14.

|

|

Principal

Accounting Fees and Services

|

|

64

|

|

|

|

|

|

|

|

PART

IV

|

|

|

|

65

|

|

Item

15.

|

|

Exhibits,

Financial Statement Schedules

|

|

65

|

PART I

CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

This

Report, including any documents which may be incorporated by

reference into this Report, contains “Forward-Looking

Statements” within the meaning of Section 27A of the

Securities Act of 1933, as amended, and Section 21E of the

Securities Exchange Act of 1934, as amended. All statements other

than statements of historical fact are “Forward-Looking

Statements” for purposes of these provisions, including our

plans of operation, any projections of revenues or other financial

items, any statements of the plans and objectives of management for

future operations, any statements concerning proposed new products

or services, any statements regarding future economic conditions or

performance, and any statements of assumptions underlying any of

the foregoing. All Forward-Looking Statements included in this

document are made as of the date hereof and are based on

information available to us as of such date. We assume no

obligation to update any Forward-Looking Statement. In some cases,

Forward-Looking Statements can be identified by the use of

terminology such as “may,” “will,”

“expects,” “plans,”

“anticipates,” “intends,”

“believes,” “estimates,”

“potential,” or “continue,” or the negative

thereof or other comparable terminology. Although we believe that

the expectations reflected in the Forward-Looking Statements

contained herein are reasonable, there can be no assurance that

such expectations or any of the Forward-Looking Statements will

prove to be correct, and actual results could differ materially

from those projected or assumed in the Forward-Looking Statements.

Future financial condition and results of operations, as well as

any Forward-Looking Statements are subject to inherent risks and

uncertainties, including any other factors referred to in our press

releases and reports filed with the Securities and Exchange

Commission. All subsequent Forward-Looking Statements attributable

to the company or persons acting on its behalf are expressly

qualified in their entirety by these cautionary statements.

Additional factors that may have a direct bearing on our operating

results are described under “Risk Factors” and

elsewhere in this report.

Introductory Comment

Throughout

this Annual Report on Form 10-K, the terms “GTBP,”

“we,” “us,” “our,” “the

company” and “our company” refer to GT Biopharma,

Inc., a Delaware corporation formerly known as DDI Pharmaceuticals,

Inc., Diagnostic Data, Inc. and Oxis International, Inc., together

with our subsidiaries.

ITEM

1. BUSINESS

We are a clinical stage

biopharmaceutical company focused on the development and

commercialization of novel immuno-oncology products based off our

proprietary Tri-specific Killer Engager (TriKE), Tetra-specific

Killer Engager (TetraKE) and bi-specific Antibody Drug Conjugate

(ADC) technology platforms. Our TriKE and TetraKE platforms

generate proprietary moieties designed to harness and enhance the

cancer killing abilities of a patient’s own natural killer,

or NK, cells. Once bound to a NK cell, our moieties are designed to

enhance the NK cell and precisely direct it to one or more

specifically-targeted proteins (tumor antigens) expressed on a

specific type of cancer, ultimately resulting in the cancer

cell’s death. TriKEs and TetraKEs are made up of recombinant

fusion proteins, can be designed to target any number of tumor

antigens on hematologic malignancies, sarcomas or solid tumors and

do not require patient-specific customization. They are designed to

be dosed in a common outpatient setting similar to modern antibody

therapeutics and are expected to have reasonably low cost of goods.

Our ADC platform generates product candidates that are bi-specific,

ligand-directed single-chain fusion proteins that, we believe,

represent the next generation of ADCs.

Our most advanced bi-specific ADC, which targets CD19+ and/or CD22+

hematological malignancies, is in a Phase 2 NHL/ALL trial, and we

plan to begin a Phase 1 trial in CD33+ hematologic malignancies for

our most advanced TriKE product candidate in the second half of

2018. We are initially targeting certain hematologic malignancies

as we believe our product candidates may have certain advantages

over existing and other in-development products. We are also

developing TetraKE product candidates designed to target the larger

solid tumor market and expect to begin human clinical trials in

2019.

We also are focused on developing a portfolio of three central

nervous system, or CNS, product candidates that are covered by

issued or filed composition of matter patents and consist of

innovative reformulations and/or repurposing of existing therapies.

We expect to take advantage of our CNS portfolio by generating

proof-of-concept data and/or achieving other milestones and

ultimately entering into strategic transactions, which may include

transactions with commercialization-oriented pharmaceutical

companies.

Our TriKE product candidates are single-chain, tri-specific scFv

recombinant fusion proteins composed of the variable regions of the

heavy and light chains (or heavy chain only) of anti-CD16

antibodies, wild-type or a modified form of IL-15 and the variable

regions of the heavy and light chains of an antibody that precisely

targets a specific tumor antigen. We utilize the NK stimulating cytokine

human IL-15 as a crosslinker between the two scFvs which provides a

self-sustaining signal that leads to the proliferation and

activation of NK cells thus enhancing their ability to kill cancer

cells mediated by antibody-dependent

cell-mediated cytotoxicity (ADCC) via the highly potent CD16

activating receptor on our moieties. Our lead TriKE, OXS-3550,

targeting CD33+ malignancies is expected to begin clinical testing

in the second half of 2018. Our second TriKE product candidate,

OXS-C3550, is a next-generation version of OXS-3550 containing a

modified CD16 component.

Our TetraKE product candidates are single-chain fusion proteins

composed of human single-domain anti-CD16 antibody, wild-type IL-15

and the variable regions of the heavy and light chains of two

antibodies that target two specific tumor antigens expressed

on specific types of cancer cells. An

example of a TetraKE product candidate is OXS-1615which targets

EpCAM and CD133 positive solid tumors. EpCAM is found on many solid

tumor cells of epithelial origin and CD133 is a marker for cancer

stem cells. OXS-1615 is designed to enable a patient’s NK

cells to kill not only the heterogeneous population of cancer cells

found in many solid tumors but also kill the cancer stem cells that

are typically responsible for recurrences. We intend to initiate

human clinical testing for certain of our solid tumor product

candidates in 2019.

Our TriKEs and TetraKEs act by binding to a patient’s NK cell

and a specific tumor antigen enabling an immune synapse between the

now IL-15-enhanced NK cell and the targeted cancer cell. The

formation of this immune synapse induces NK cell activation leading

to the death of the cancer cell. The self-sustaining signal caused

by our IL-15 cross-linker enables prolonged and enhanced

proliferation and activation of NK cells similar to the increased

proliferation of T-cells caused by 41BB-L or CD28 intracellular

domains in CAR-T therapy but without the need to enhance the

patient’s NK cells ex vivo.

We are using our TriKE and TetraKE platforms with the intent to

bring to market multiple immuno-oncology products that can treat a

wide range of hematologic malignancies, sarcoma and solid tumors.

The platforms are scalable and we are putting processes in place to

be able to produce IND-ready moieties in approximately 90-120 days

after a specific TriKE or TetraKE conceptual design. After

conducting market and competitive research, specific moieties can

then be rapidly advanced into the clinic on our own or through

potential collaborations with larger companies. We are currently

evaluating over a dozen moieties and intend to announce additional

clinical product candidates in the second half of 2018. We believe

our TriKEs and TetraKEs will have the ability, if approved for

marketing, to be used on a stand-alone basis, augment the current

monoclonal antibody therapeutics, be used in conjunction with more

traditional cancer therapy and potentially overcome certain

limitations of current chimeric antigen receptor, or CAR-T,

therapy.

We also believe our bi-specific, ligand-directed single-chain

fusion proteins represents the next generation of ADCs. Our lead

bi-specific ADC, OXS-1550, which targets CD19+ and/or CD22+

hematological malignancies is currently in a Phase 2 trial being

conducted at the University of Minnesota Masonic Cancer Center in

patients with relapsed/refractory B-cell leukemias or lymphomas. We

believe OXS-1550 has certain properties that could result in

competitive advantages over recently approved ADC products

targeting leukemias and lymphomas. In a Phase 1 trial, of nine

patients that achieved adequate blood levels, we saw a durable

complete response, or CR, in two heavily pretreated patients. One

patient, who had failed multiple previous treatment regimens, has

been cancer free since early 2015.

Our initial work has been conducted in collaboration with the

Masonic Cancer Center at the University of Minnesota under a

program led by Dr. Jeffrey Miller, the Deputy Director. Dr. Miller

is a recognized leader in the field of NK cell and IL-15 biology

and their therapeutic potential. We have exclusive rights to the

TriKE and TetraKE platforms and are generating additional

intellectual property around specific moieties.

We also are focused on developing a portfolio of central nervous

system, or CNS, product candidates that are covered by formulation

patents and issued or filed composition of matter patents and

consist of innovative reformulations and/or repurposing of existing

therapies. We believe our CNS product candidates represent

potentially near-to-market opportunities that may have broader

potential applicability beyond their initial indication. Certain

members of our management team have a track-record of developing

CNS products and product candidates with similar strategies

including at Chase Pharmaceuticals and Prestwick Pharmaceuticals.

We have designed our CNS clinical programs with the intent to

efficiently advance each program to an FDA New Drug Application in

a certain initial indication and expand applicable markets

potentially after approval. Our three product candidates are

initially targeting a rare autoimmune disease Myasthenia Gravis, a

rare neuropathic pain indication, trigeminal neuralgia, and a

vestibular disorder, motion sickness.

Immuno-Oncology Platform

Tri-specific Killer Engagers (TriKEs) and Tetra-specific Killer

Engagers (TetraKEs)

The generation of chimeric antigen receptor, or CAR, expressing T

cells from monoclonal antibodies has represented an important step

forward in cancer therapy. These therapies involve the genetic

engineering of T cells to express either CARs, or T cell receptors,

or TCRs, and are designed such that the modified T cells can

recognize and destroy cancer cells. While a great deal of interest

has recently been placed upon chimeric antigen receptor T, or

CAR-T, therapy, it has certain limitations for broad potential

applicability because it can require an individual approach that is

expensive and time consuming, and may be difficult to apply on a

large scale. We believe there is an unmet need for targeted

immuno-oncology therapies that have the potential to be dosed in a

patient-friendly outpatient setting, can be used on a stand-alone

basis, augment the current monoclonal antibody therapeutics and/or

be used in conjunction with more traditional cancer therapy. We

believe our TriKE and TetraKE constructs have this potential and

therefore we have generated, and intend to continue to generate, a

pipeline of product candidates to be advanced into the clinic on

our own or through potential collaborations with larger

companies.

NK cells represent an important immunotherapeutic target as they

are involved in tumor immune-surveillance, can mediate

antibody-dependent cell-mediated cytotoxicity (ADCC), contain

pre-made granules with perforin and granzyme B and can quickly

secrete inflammatory cytokines, and unlike T cells they do not

require antigen priming and can kill cells in the absence of major

histocompatibility complex (MHC) presentation.

Unlike full-length antibodies, TriKEs and TetraKEs are small

single-chain fusion proteins that bind the CD16 receptor of NK

cells directly producing a potent and lasting response, as

demonstrated by preclinical studies. An additional benefit they may

have is attractive biodistribution, as a consequence of their

smaller size, which we expect to be important in the treatment of

solid tumors. In addition to these advantages, TriKEs and TetraKEs

are designed to be non-immunogenic, have appropriate clearance

properties and can be engineered quickly to target a variety of

tumor antigens.

Background and Select Non-Clinical Data

In conjunction with our research agreement with the Masonic Cancer

Center at the University of Minnesota, the exploration of targeting

NK cells to a variety of tumors initially focused on novel

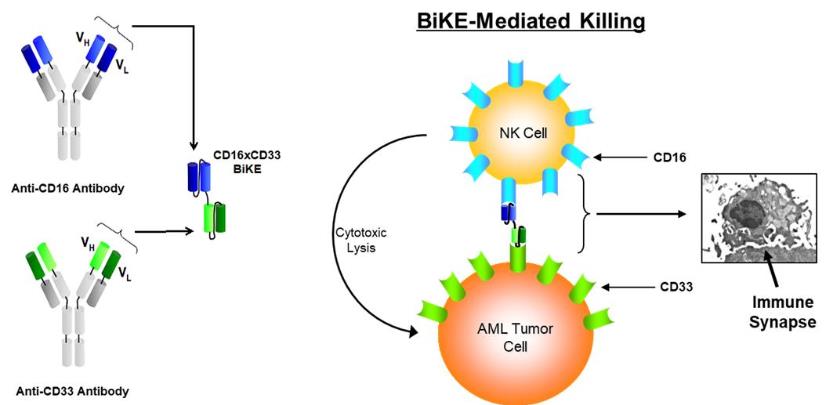

bi-specific killer engagers, or BiKEs, composed of the variable

portions of antibodies targeting the CD16 activating receptor on NK

cells and CD33 (AML and MDS; see figure below), CD19/CD22 (B cell

lymphomas), or EpCAM (epithelial tumors (breast, colon, and lung))

on the tumor cells.

Subsequently, a tri-specific (TriKE) construct that replaced the

linker molecule between the CD16 scFv and the CD33 scFv with a

modified IL-15 molecule, containing flanking sequences, was

generated and tested. Data indicate that the CD16 x IL-15 x CD33

and CD16 x IL-15 x EpCAM TriKEs potently induce proliferation of

healthy donor NK cells, possibly greater than that induced by

exogenous IL-15, which is absent in the BiKE platform. Targeted

delivery of the IL-15 through the TriKE also resulted in specific

expansion of the NK cells without inducing T cell expansion on

post-transplant patient samples.

When compared to the CD16 x CD33 BiKE, the CD16 x IL-15 x CD33

TriKE is also capable of potently restoring killing capacity of

post-transplant NK cells against CD33-expressing HL-60 Targets and

primary AML blasts. These results demonstrated the ability to

functionally incorporate an IL-5 cytokine into the BiKE platform

and also demonstrated the possibility of targeting a variety of

cytokines directly to NK cells while reducing off-target effects

and the amount of cytokines needed to obtain biologically relevant

function.

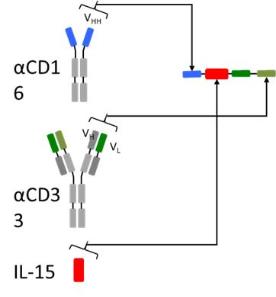

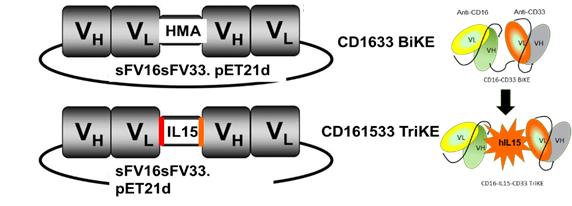

The figure below is a schematic of a BiKE construct (top) and a

TriKE construct (bottom), which has the modified IL-15 linker

between the CD16 scFv and the CD33 scFv components.

The TriKE constructs were also tested against three separate human

tumor cell lines: HL-60 (promyelocitic leukemia), Raji

(Burkitt’s lymphoma), and HT29 (colorectal adenocarcinoma),

in addition to a model for ovarian cancer. All cell lines contained

the Luc reporter to allow for in vivo imaging of the tumors. These

systems were used to show in vivo efficacy of BiKEs (1633) and

TriKEs (OXS-3550) against relevant human tumor targets (HL-60-luc)

over an extended period of time. The system consisted of initial

conditioning of mice using radiation (250-275 cGy), followed by

injection of the tumor cells (I.V. for HL-60-luc and Raji-luc,

intra-splenic for HT29-luc and IP for ovarian for MA-148-luc), a

three-day growth phase, injection of human NK cells, and repeated

injection of the drugs of interest, BiKE and TriKE (three to five

times a week). Imaging was carried out at day 7, 14, and 21, and

extended as needed.

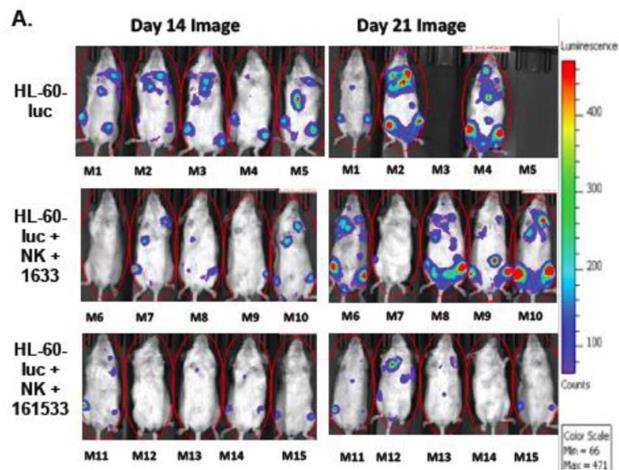

Figure A below shows the results (tumor burden and mortality) when

dosing NK cells alone (top panel), the BiKE version (lacking IL-15)

of OXS-3550 (middle panel; called 1633), and the TriKE, OXS-3550

(bottom panel; then called 161533) in the above described human

tumor model, HL-60-luc. In the NK-cell-only arm, two out of the

five mice were dead by day 21 with two of the surviving mice having

extensive tumor burden as depicted by the colored images. In

contrast, all five mice in each of the BiKE and TriKE arms

survived. In addition, the tumor burden in the TriKE-treated mice

was significantly less than in the BiKE-treated mice, demonstrating

the improved efficacy from NK cells in the TriKE-treated

mice.

Based on these results, and others, the IND for OXS-3550 was filed

in June 2017 by the University of Minnesota. FDA requested that

additional nonclinical toxicology be conducted prior to initiating

clinical trials. The FDA also requested some additional information

and clarifications on the manufacturing (CMC) and clinical

packages. We plan to incorporate the requested additional

toxicology studies, information and clarifications in

the IND that was transferred to us from the University of

Minnesota in October 2017. We expect to begin a Phase 1 clinical

trial for OXS-3550 in the second half of 2018.

Generation of humanized single-domain antibody targeting CD16 for

incorporation into the TriKE platform

To develop second generation TriKEs, we designed a new humanized

CD16 engager derived from a single-domain antibody. While scFvs

consist of a heavy and a light variable chain joined by a linker,

single-domain antibodies consist of a single variable heavy chain

capable of engaging without the need of a light chain counterpart

(see figure below).

These single-domain antibodies are thought to have certain

attractive features for antibody engineering, including physical

stability, ability to bind deep grooves, and increased production

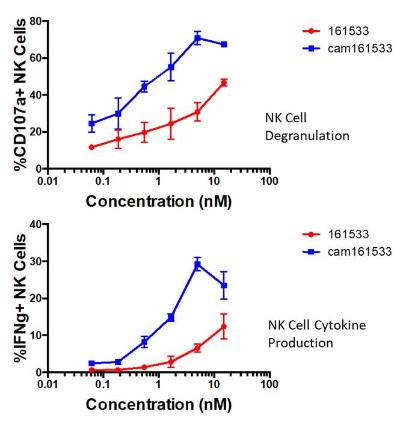

yields, amongst others. Pre-clinical studies demonstrated increased

activity (NK Cell Degranulation) and functionality (NC Cell

Cytokine Production) of the single-domain CD16 TriKE (OXS-C3550)

compared to the original TriKE (OXS-3550) (see figure below). These

data were presented at the 2017 American Society of Hematology

Conference.

Targeting Solid Tumors and Other Potentially Attractive

Characteristics

Unlike full-length antibodies, TriKEs and TetraKEs are small

single-chain fusion proteins that bind the CD16 receptor of NK

cells directly producing a potentially more potent and lasting

response as demonstrated by preclinical studies. An additional

benefit that they may have is an attractive biodistribution,

because of their smaller size, which we expect to be important in

the treatment of solid tumors. In addition to these potential

advantages, TriKEs and TetraKEs are designed to be non-immunogenic,

have appropriate clearance properties and can be engineered quickly

to target a variety of tumor antigens. We believe these attributes

make them an ideal pharmaceutical platform for potentiated NK

cell-based immunotherapies and have the potential to overcome some

of the limitations of CAR-T therapy and other antibody

therapies.

Examples of our earlier stage solid tumor targeting product

candidates are focused on EpCAM, Her2, Mesothelin (mesothelioma and

lung adenocarcinoma), and CD133 alone and in combination. We

believe certain of these constructs have the potential to target

prostate, breast, colon, ovarian, liver, and head and neck cancers.

We intend to initiate human clinical testing for certain of our

solid tumor product candidates in 2019.

Efficient Advancement of Potential Future Product Candidates

--Production and Scale Up

We are using our TriKE and TetraKE platforms with the intent to

bring to market multiple immuno-oncology products that can treat a

range of hematologic malignancies, sarcomas and solid tumors. The

platforms are scalable and we are currently working with several

third parties investigating the optimal expression system of the

TriKEs and TetraKE constructs which we expect to be part of a

process in which we are able to produce IND-ready moieties in

approximately 90-120 days after the construct conceptual

design.

After conducting market and competitive research, specific moieties

can then be rapidly advanced into the clinic on our own or through

potential collaborations with larger companies. We are currently

evaluating over a dozen moieties and intend to announce additional

clinical product candidates in the second half of

2018.

We believe our TriKEs and TetraKEs will have the ability, if

approved for marketing, to be used on a stand-alone basis, augment

the current monoclonal antibody therapeutics, or be used in

conjunction with more traditional cancer therapy and potentially

overcome certain limitations of current chimeric antigen receptor,

or CAR-T, therapy.

Bi-specific Antibody-Drug Conjugates Program

Antibody–drug conjugates (ADCs) are a class of potent

biopharmaceutical drugs designed as a targeted therapy for the

treatment of cancer. ADCs combine the antitumor potency

of highly cytotoxic small-molecule drugs with the high selectivity,

pharmacokinetic profile of mAbs. These attributes allow sensitive

discrimination between healthy and diseased tissue. We believe our

bi-specific, ligand-directed single-chain fusion protein represents

an example of the next generation of ADCs.

OXS-1550, our bi-specific ADC, is a single chain bispecific

recombinant fusion protein consisting of an anti-CD22 sFv, an

anti-CD19 sFv, and DT390 (the catalytic and translocation domains

of diphtheria toxin). It is a cytotoxic molecule produced by

recombinant DNA techniques composed of a fusion gene consisting of

sequences for DT390 and also sequences encoding two separate and

distinct sFvs, one recognizing CD22 and one recognizing CD19. The

anti-CD22 sFv comes from the monoclonal antibody RFB4 and this sFv

is currently in clinical trials involving another anti-CD22

immunotoxin called BL22. The anti-CD19 sFv is from the monoclonal

antibody HD37 that has previously been used clinically. Published

preclinical studies have shown that the presence of both sFvs on

the same single chain molecule results in a bispecific fusion toxin

that has superior activity and anti-cancer effects compared to the

monospecific fusion toxins. Between the VL and VH regions of the

sFvs, we have introduced aggregation reducing sequences (ARL) which

has produced a product which has demonstrated better activity

against scid mouse systemic models of B cell malignancy. The action

of DT2219 occurs as a result of binding to the CD22 and/or CD19

receptors, subsequent internalization, and enzymatic inhibition of

protein synthesis leading to cell death.

We believe that our single-chain bi-specific recombinant fusion

proteins utilizing novel linkers and innovative warheads represent

an important advance over currently marketed ADCs. Utilizing our

bi-specific ADC platform we have the ability to generate novel ADCs

with unique targets, linkers and warheads. This platform provides

us with the ability to rapidly construct novel ADCs with the

potential to treat a wide range of cancers, including hematologic

and solid tumors.

Immuno-Oncology Product Candidates

OXS-1550

OXS-1550 is a bispecific scFv recombinant fusion protein-drug

conjugate composed of the variable regions of the heavy and light

chains of anti-CD19 and anti-CD22 antibodies and a modified form of

diphtheria toxin (DT390) as its cytotoxic drug payload. CD19

is a membrane glycoprotein present on the surface of all stages of

B-lymphocyte development and is also expressed on most B-cell

mature lymphoma cells and leukemia cells. CD22 is a

glycoprotein expressed on B-lineage lymphoid precursors, including

precursor acute lymphoblastic leukemia, and often is co-expressed

with CD19 on mature B-cell malignancies such as

lymphoma.

OXS-1550 targets cancer cells expressing the CD19 receptor or CD22

receptor or both receptors. When OXS-1550 binds to cancer

cells, the cancer cells internalize OXS-1550, and are killed due to

the action of drug’s cytotoxic diphtheria toxin

payload. OXS-1550 has completed a Phase 1 human clinical

trial in patients with relapsed/refractory B-cell lymphoma or

leukemia.

The initial Phase 1 study enrolled 25 patients with mature or

precursor B-cell lymphoid malignancies expressing

the CD19 receptor or CD22 receptor or

both receptors. All 25 patients

received at least a single course of therapy. The treatment at the

higher doses produced objective tumor responses with one patient in

continuous partial remission and the second in complete remission.

A Phase 2 trial of OXS-1550 is underway in patients with ALL/NHL.

The FDA-approved clinical trial is being conducted at the

University of Minnesota's Masonic Cancer Center. There are

currently 18 patients enrolled in this clinical trial. Patients in

this trial are given an approved increased dosage and schedule of

OXS-1550.

We began enrolling patients in Phase 2 trial of OXS-1550 during the

first quarter of 2017 and the first patient began dosing in April

2017. We expect data from this

Phase 2 trial to be available in the second half

2018.

OXS-3550

OXS-3550 is our first TriKE product candidate. It is a

single-chain, tri-specific scFv recombinant fusion protein

conjugate composed of the variable regions of the heavy and light

chains of anti-CD16 and anti-CD33 antibodies and a modified form of

IL-15. We intend to study this anti-CD16-IL-15-anti-CD33

TriKE in CD33 positive leukemias, a marker expressed on tumor cells

in acute myelogenous leukemia, or AML, myelodysplastic syndrome, or

MDS, and other hematopoietic malignancies. CD33 is primarily a

myeloid differentiation antigen with endocytic properties broadly

expressed on AML blasts and, possibly, some leukemic stem cells.

CD33 or Siglec-3 (sialic acid binding Ig-like lectin 3, SIGLEC3,

SIGLEC3, gp67, p67) is a transmembrane receptor expressed on cells

of myeloid lineage. It is usually considered myeloid-specific, but

it can also be found on some lymphoid cells. The anti-CD33 antibody

fragment that will be used for these studies was derived from the

M195 humanized anti-CD33 scFV and has been used in multiple human

clinical studies. It has been exploited as target for therapeutic

antibodies for many years. We believe the recent approval of the

antibody-drug conjugate gemtuzumab validates this targeted

approach.

The

OXS-3550 IND will focus on AML, the most common form of adult

leukemia with 21,000 new cases expected in 2018 alone (American

Cancer Society). These patients typically receive frontline

therapy, usually chemotherapy, including cytarabine and an

anthracycline, a therapy that has not changed in over 40 years.

About half will have relapses and require alternative therapies. In

addition, MDS incidence rates have dramatically increased in the

population of the United States from 3.3 per 100,000 individuals

from 2001-2004 to 70 per 100,000 annually, MDS is especially

prevalent in elderly patients that have a median age of 76 years at

diagnosis. The survival of patients with MDS is poor due to

decreased eligibility, as a result of advanced age, for allogeneic

hematopoietic cell transplantation (Allo-HSCT), the only curative

MDS treatment (Cogle CR. Incidence and Burden of the

Myelodysplastic Syndromes. Curr

Hematol Malig Rep. 2015; 10(3):272-281). We expect OXS-3550

could serve as a relatively safe, cost-effective, and easy-to-use

therapy for resistant/relapsing AML and could also be combined with

chemotherapy as frontline therapy thus targeting the larger

market.

The IND for OXS-3550 was filed in June 2017 by the University of

Minnesota. FDA requested that additional preclinical toxicology be

conducted prior to initiating clinical trials. The FDA also

requested some additional information and clarifications on the

manufacturing (CMC) and clinical packages. The

requested additional toxicology studies, information

and clarifications will be incorporated by our company in

the IND that was transferred to us from the University of

Minnesota in October 2017. We expect to begin a Phase 1 clinical

trial in the second half of 2018.

OXS-C3550

OXS-C3550 is a next-generation, follow-on, to our lead TriKE,

OXS-3550. OXS-C3550 contains a modified CD16 moiety which has

improved binding characteristics and enhanced tumor cell killing

based on functional assays and animal models of AML. Using our

platform technology, we substituted the anti-CD16 scFv arm in

OXS-3550 with a novel humanized single-domain anti-CD16 antibody to

create this second-generation molecule which may have improved

functionality. Single-domain antibodies, such as OXS-C3550,

typically have several advantages, including better stability and

solubility, more resistance to pH changes, can better recognize

hidden antigenic sites, lack of a VL

portion thus preventing

VH/VL

mispairing and are suitable for

construction of larger molecules. OXS-C3550 induced a potent

increase in NK cell degranulation, measured by CD107a expression

against HL-60 AML tumor targets when compared to our

first-generation TriKE (70.75±3.65% vs. 30.75±5.05%).

IFN production was similarly enhanced (29.2±1.8%

vs. 6.55±1.07%). OXS-C3550 also exhibited a robust increase in

NK cell proliferation (57.65±6.05% vs.

20.75±2.55%).

OXS-3550 studies will help inform the development of OXS-C3550

which we expect will de-risk the OXS-C3550 program as data will be

generated to make an informed decision on which, or both, will be

brought into later phase studies.

OXS-1615

OXS-1615 is an example of our first-generation TetraKEs designed

for the treatment of solid tumors. It is a single-chain fusion

protein composed of CD16-IL15-EpCAM-CD133. EpCAM is found on many

solid tumor cells of epithelial origin and CD133 is a marker for

cancer stem cells. This TetraKE is designed to target not only the

heterogeneous population of cancer cells found in solid tumors but

also the cancer stem cells that are typically responsible for

recurrences. We intend to initiate human clinical testing for

certain of our solid tumor product candidates in 2019.

Central Nervous System

Our CNS portfolio consists of innovative reformulations and/or

repurposing of existing therapies and are covered by issued

formulation or filed composition of matter patents (PCTs and

provisionals). We believe our CNS product candidates address

numerous unmet medical needs that can lead to improved efficacy

and/or address tolerability and safety issues that tend to limit

the usefulness of the original approved drug. Our CNS drug

candidates address disease states such as chronic neuropathic pain

(trigeminal neuralgia), myasthenia gravis and vestibular

disorders.

In January 2018, we completed dosing in our Phase 1 clinical trial

for GTP-004, our product candidate for the treatment for the

symptoms of myasthenia gravis. Based on the data, and discussions

with key opinion leaders, we expect to be in a position to initiate

a Phase 2 clinical trial in patients in the second half of

2018.

We also began a proof-of-concept

clinical trial for GTP-011, a 72-hour patch for the prevention of

motion sickness, in late February 2018. We anticipate that the new

drug application, or NDA, will be a 505(b)2 NDA for each of these

programs. PainBrake®

is designed to enable accurate dose fractionation for the treatment

of certain forms of neuropathic pain and we expect to complete the manufacturing tablets for

a bioequivalence study in the second half of 2018 and to conduct a

bioequivalence study subsequently.

CNS Product Candidates

GTP-004

GTP-004

is a fixed-dose combination tablet for the treatment of the muscle

weakness associated with myasthenia gravis, or MG, a chronic

autoimmune disease of the neuromuscular junction characterized by

muscle weakness. MG affects an estimated approximately 36,000 to

60,000 people in the U.S. The basic

abnormality in MG is a reduction in nicotinic acetylcholine

receptors (AChRs) or neighboring proteins at the neuromuscular

junctions (Drachman, 2016). In neonatal myasthenia, the fetus may

acquire antibodies from a mother affected with MG. Generally, cases

of neonatal MG are temporary and the child's symptoms usually

disappear within 2-3 months after birth (Myasthenia Gravis Fact

Sheet; National Institute of neurological Disorders and Stroke,

2016). Rarely, children may have congenital myasthenic syndrome

(CMS) caused by defective gene mutations (Engel, 2012). In some

cases, degeneration of the nerves that innervate muscles such as

occurs with aging (Lexel, 1997) leads to a myasthenic syndrome.

Recently (Makarious et al, 2017), have reported on a myasthenic

syndrome associated with the use of checkpoint

inhibitors.

Cholinesterase

inhibitors, or ChEIs, that do not get into the brain (do not cross

the blood-brain barrier), such as pyridostigmine and neostigmine are used to

treat the muscular weakness associated with myasthenia gravis and

other myasthenic syndromes).

However, ChEIs also act at cholinergic synapses in the gut to cause

GI side effects such as diarrhea, nausea and vomiting, which are

dose-limiting (Engel 2012; Abicht et

al, 2003 updated in 2014).

GTP-004

combines pyridostigmine with ondansetron, designed to attenuate the

gastrointestinal, or GI, side effects of pyridostigmine alone.

Mitigating the GI side effects of pyridostigmine with a drug that

prevents diarrhea, nausea and vomiting should lead to greater

patient comfort, safety, and compliance as well as to improved

efficacy. Several provisional patent applications protecting the

combination of neostigmine or pyridostigmine with a number of

antiemetic drugs were filed by GTP in early 2017.

GTP-004

completed dosing in a Phase 1 clinical trial in January 2018. The

objective of the Phase 1 clinical trial was to demonstrate

that GI side effects of pyridostigmine are reduced with GTP-004.

Healthy volunteers were enrolled in the Phase 1 study.

Following enrollment, subjects received single increasing oral

doses of pyridostigmine (ranging from 30 to 120mg) administered

once daily in the morning. Once subjects experienced intolerable

GI side effects and reached First Intolerable Dose -FID1- as

defined by protocol criteria, upward dose escalation of

pyridostigmine was discontinued and subjects were washed out for 2

to 7 days. Next, subjects that reached FID received daily

increasing doses of pyridostigmine in combination with

ondansetron.

Three

subjects (2 males, one female; aged 34 to 43) reached intolerable

gastrointestinal side effects with pyridostigmine alone. The

dose-limiting gastro-intestinal adverse event occurred at 60 mg for

2 subjects, and 90 mg for the third subject. When these three

subjects received GTP-004 (pyridostigmine with ondansetron),

gastro-intestinal adverse events were abrogated, and all subjects

tolerated doses as high as 120 mg, the maximum allowed dose allowed

by the protocol.

Based

on the data from the Phase 1 clinical trial, and discussions with

key opinion leaders, we expect to be in a position to initiate a

Phase 2 clinical trial in patients in the second half of

2018.

Provisional

patent applications protecting the combination of

Mestinon®

or Prostigmine®

with a number of antiemetic drugs were filed by GTP in early

2017.

PainBrake

PainBrake

is a new patented formulation of carbamazepine

(Tegretol®)

that enables accurate dose fractionation for the treatment of

neuropathic pain, a condition that results from a dysfunction of

nerves involved in the perception of pain and that is typically

chronic and particularly prevalent in elderly patients. An

NIH-supported study published in 2009 estimated that almost 16

million Americans suffer from chronic neuropathic pain (Yawn et

al., 2009) and this number is expected to increase due to the aging

population. Current drugs provide a useful degree of pain relief in

only about half the patients, very few patients achieve complete

relief of pain (Nightingale, 2012). Peak dose-limiting side

effects, mainly sedation, somnolence, dizziness and balance

problems which are poorly tolerated by the elderly (Oomens et al.,

2015) cause patients to be under-dosed, thereby contributing to

inadequate pain relief. This is particularly true for

carbamazepine, a drug that is considered to be the first line

therapy for the treatment of certain forms of neuropathic pain

(Zakrzewska, 2015).

To

overcome dose-limiting side effects, PainBrake tablets employ an

innovative bilayered, deeply scored design patented by AccuBreak.

The top layer contains carbamazepine and is pre-divided by deep

scoring during the manufacturing process to provide accuracy of

dose adjustments by enabling easy tablet splitting into exact

doses. The bottom layer provides mechanical stability and serves as

the break region when splitting the tablet. We have in-licensed against milestones and royalties

the worldwide rights to the use of the AccuBreak technology for the

delivery of drugs that like carbamazepine are voltage-gated sodium

channel blockers. The core patent for the AccuBreak

technology expires in 2025.

PainBrake®

is designed to enable accurate dose fractionation for the treatment

of certain forms of neuropathic pain and we expect to complete the manufacturing tablets for

a bioequivalence study in the second half of 2018 and to begin a

bioequivalence study as a subsequent step.

GTP-011

We are

developing GTP-011 as a 72-hour transdermal product for the

prevention of motion sickness, a well-known syndrome that typically

involves nausea and vomiting in otherwise healthy people and that

occurs upon exposure to certain types of motion.

Currently, the scopolamine patch (Transderm Scop®

from Novartis) is viewed as a

first-line medication for prevention of motion sickness (Gil et

al., 2012; Brainard and Gresham, 2014). However, side effects can

be of particular concern and include sedation (Spinks et al.,

2004), reduced memory for new information, impaired attention, and

lowered feelings of alertness (Parrott, 1989). Mental confusion or

delirium can occur after application of scopolamine patch (Seo et

al., 2009). Elderly people as well as people with undetected

incipient dementia or mild cognitive impairment, or MCI, may be

particularly prone to develop mental confusion after applying the

scopolamine patch (Seo et al., 2009).

GTP-011,

like scopolamine, is a transdermal formulation that contains a

muscarinic receptor antagonist. Unlike scopolamine, however,

GTP-011’s active ingredient has been reported not to affect

memory and cognition and has a low incidence of sedation

(Kay et al., 2012). GTP-011 may

thus be a more favorable alternative, if approved for marketing, to

the scopolamine patch for the treatment of motion sickness. Since

GTP-011 is expected to be a new formulation of an approved drug, we

anticipate that the NDA will be a 505(B)2 NDA. We began a proof-of-concept clinical trial for

GTP-011 in late February 2018.

Our Strategy

Our goal is to be a leader in immuno-oncology therapies targeting a

broad range of indications including hematological malignancies,

sarcoma and solid tumors and to generate value from our CNS product

candidates. Key

elements of our strategy are to:

Expedite clinical development, regulatory approval and

commercialization of our bi-specific ADC, OXS-1550, in specific

indications with a high unmet-medical need such as patients who are

resistant or refractory to conventional treatment and also assess

fast-to-market strategies in potential orphan indications

Based upon promising clinical results from the initial OXS-1550

Phase 1 study, we began enrolling patients in a Phase 2 trial

during the first quarter of 2017 for our most advanced oncology

product candidate, OXS-1550, for the treatment of patients with

relapsed/refractory B-cell leukemias or lymphomas. In the Phase 1

study, of the nine patients who received OXS-1550 at the higher

doses, two had durable complete responses in heavily pretreated

patients. One of these patients, who had failed multiple previous

treatment regimens, has been cancer free since the beginning of

2015.

The approximately 34 patient, open label, two stage, FDA-approved

Phase 2 trial is being conducted at the University of Minnesota's

Masonic Cancer Center. The trial is a continuation of the dose and

schedule finding component of the Phase 1 study using the dose

limiting toxicity identified in the Phase 1 but with a higher

number of cycles. The trial is designed to confirm the safety of

OXS-1550 and make a preliminary determination of activity level by

disease. There

are currently 18 patients enrolled in the Phase 2 trial and

we expect data from this Phase 2 trial

to be available in the second half 2018.

We will also utilize our bi-specific ADC platform to generate novel

ADCs with unique targets, linkers and warheads. We anticipate that

this platform will give us the ability to rapidly construct novel

ADCs with the potential to treat a wide range of cancers, including

hematologic and solid tumors.

Rapidly advanced our Tri-specific Killer Engagers (TriKEs),

OXS-3550 and OXS-C3550

Our

TriKE and TetraKE product candidates have the potential to be

groundbreaking therapies targeting a broad range of hematologic

malignancies, sarcomas and solid tumors. We are preparing to study

OXS-3550, an anti-CD16-IL-15-anti-CD33 TriKE in CD33 positive

leukemias, a marker expressed on tumor cells in AML, MDS and other

myeloid malignancies. We expect to begin a Phase 1 clinical trial

in the second half of 2018 in patients with relapsed/refractory

AML. The Phase 1 trial will be a dose finding study. We expect this

will be closely followed by Phase 2 trials to determine the most

efficacious dosing and cycles with the aim to maximize efficacy

while minimizing on-target, off-disease adverse

events.

OXS-C3550 contains a humanized single-domain anti-CD16 moiety which

demonstrated improved binding characteristics and enhanced tumor

cell killing based on functional assays and animal models of

AML.

We have

designed OXS-3550 and OXS-C3550, if approved for marketing, to

serve as a relatively safe, cost-effective, and easy-to-use

therapies for resistant/relapsing AML or MDS which could also be

combined with chemotherapy as frontline therapy thus targeting a

broad AML/MDS market.

OXS-C3550 is a next-generation, follow-on, to our lead TriKE,

OXS-3550. OXS-3550 studies will help inform the development of

OXS-C3550. We believe this will de-risk the OXS-C3550 program as

the data being generated will help to make informed decisions on

which, or both, will be brought into later phase studies and in

which patient populations.

Utilize our TriKE and TetraKE platform technologies to develop a

robust pipeline of targeted immuno-oncology products targeting a

wide range of hematologic malignancies, sarcomas and solid tumors

for development on our own and through potential collaborations

with larger pharmaceutical companies

We are using our TriKE and TetraKE platforms with the intent to

bring to market multiple, targeted, off-the-shelf therapies that

can treat a range of hematologic malignancies, sarcomas and solid

tumors. The platforms are scalable and we are currently working

with several third parties investigating the optimal expression

system of the TriKEs and TetraKE constructs which we expect to be

part of a process in which we are able to produce IND-ready

moieties in approximately 90-120 days after the construct

conceptual design. After conducting market and competitive

research, specific moieties can then be rapidly advanced into the

clinic on our own or through potential collaborations with larger

pharmaceutical companies.

We are currently evaluating over a dozen moieties and intend to

announce additional clinical product candidates in the second half

of 2018. We intend to initiate human clinical testing for certain

of our solid tumor product candidates in 2019.

We believe our TriKEs and TetraKEs will have the ability, if

approved for marketing, to be used on a stand-alone basis, augment

the current monoclonal antibody therapeutics, or be used in

conjunction with more traditional cancer therapy and potentially

overcome certain limitations of current chimeric antigen receptor,

or CAR-T, therapy.

Continue our collaborative relationship with the Masonic Cancer

Center at the University of Minnesota, under a program led by Dr.

Jeffrey Miller and become the leading NK-oriented

immune-oncology company

We believe that the TriKE and TetraKE constructs represent

potentially groundbreaking innovations in immunotherapy. In July

2016 we entered into an exclusive license agreement with the

University of Minnesota to

develop and commercialize cancer therapies using TriKE and TetraKE

technology developed by researchers at the university to target NK

cells to cancer.

We believe TriKE and TetraKE therapeutics have the potential to

significantly impact the standard of care for hematologic

malignancies, sarcomas, as well as solid tumors. The direct

engagement of the NK cell with the tumor cell via very specific

receptors may increase the efficacy while decrease the toxicity

seen with other forms of immunotherapies. If approved, we expect

the TriKEs and TetraKEs will be able to be administered at cancer

treatment facilities without the need for specialized centers or

product-specific trained staff.

We also intend to selectively evaluate and potentially acquire or

enter into licensing or other agreements for technologies and/or

product candidates that we believe would complement our oncology

product candidates and platform technologies.

Monetize our CNS programs through transactions with

commercialization-oriented pharmaceutical companies and/or other

transactions

Our CNS portfolio consists of innovative reformulations and/or

repurposing of existing therapies and are covered by formulation

patents or filed composition of matter patents (PCTs and

provisional applications) and represent, what we believe to be,

near-to-market product opportunities. Our CNS programs address

numerous unmet medical needs that, if approved, we believe may lead

to improved efficacy while addressing tolerability and safety

issues that tend to limit the usefulness of the original approved

drugs.

We expect to take advantage of our CNS portfolio by generating

proof-of-concept data and/or achieving other milestones and

ultimately entering into transactions with

commercialization-oriented pharmaceutical companies, which could

result in income, or enter into other transaction structures with

the intent to generate value for our shareholders.

Oncology Markets

B-cell Lymphomas/Leukemias

B-cell

lymphoma is a type of cancer that forms in B cells (a type of

immune system cell). Bcell lymphomas may be either indolent

(slow-growing) or aggressive (fast-growing). Most Bcell

lymphomas are non-Hodgkin lymphomas. There are many different types

of B-cell non-Hodgkin lymphomas. These include Burkitt lymphoma,

chronic lymphocytic leukemia/small lymphocytic lymphoma (CLL/SLL),

diffuse large B-cell lymphoma, follicular lymphoma, and mantle cell

lymphoma. It is the most common type of non- Hodgkin lymphoma among

adults, with an annual incidence of 7–8 cases per 100,000

people per year.

Acute Lymphoblastic Leukemia

Acute

lymphoblastic leukemia, or ALL, is an acute form of leukemia, or cancer of the

white blood cells, characterized by the overproduction and

accumulation of immature white blood cells, known as lymphoblasts.

In persons with ALL, lymphoblasts are overproduced in the bone

marrow and continuously multiply, causing damage and death by

inhibiting the production of normal cells (such as red and white

blood cells and platelets) in the bone marrow and by spreading

(infiltrating) to other organs.

It is

estimated that there will be approximately 6,000 new cases of ALL

reported in the United States in 2018 (ACS Cancer Facts &

Figures 2018). "Acute" is defined by the World Health Organization

standards, in which greater than 20% of the cells in the bone

marrow are blasts. Chronic lymphocytic leukemia is defined as

having less than 20% blasts in the bone marrow. Acute lymphoblastic

leukemia is seen in both children and adults; the highest incidence

is seen between ages 2 and 5 years. ALL is the most common

childhood cancer constituting about 23 to 30% of cancers before age

15. Although 80 to 90% of children will have a durable complete

response with treatment it is the leading cause of cancer-related

deaths among children.

Multiple Myeloma

Multiple

myeloma is a type of cancer that forms in white blood cells and

will affect an estimated 30,770 people in 2018 in the U.S. causing

about 12,770 deaths. Multiple myeloma causes cancer cells to

accumulate in the bone marrow, where they crowd out healthy blood

cells. Multiple myeloma is also characterized by destructive lytic

bone lesions (rounded, punched-out areas of bone), diffuse

osteoporosis, bone pain, and the production of abnormal proteins

which accumulate in the urine. Anemia is also present in most

multiple myeloma patients at the time of diagnosis and during

follow-up. Anemia in multiple myeloma is multifactorial and is

secondary to bone marrow replacement by malignant plasma cells,

chronic inflammation, relative erythropoietin deficiency, and

vitamin deficiency. Plasma cell leukemia, a condition in which

plasma cells comprise greater than 20% of peripheral leukocytes, is

typically a terminal stage of multiple myeloma and is associated

with short survival.

Myeloid Leukemias

Acute Myeloid Leukemia

AML is a heterogeneous hematologic stem cell malignancy in adults

with incidence rate of 3–5% per 100,000 populations. The

median age at the time of diagnosis is 65–69 years. AML is an

aggressive disease and is fatal without anti-leukemic treatment.

AML is the most common form of adult leukemia with 20,000 new cases

each year. These patients will require frontline therapy, usually

chemotherapy including cytarabine and an anthracycline, a therapy

that has not changed in over 40 years. Myelodysplastic syndromes

(MDS) are a heterogeneous group of myeloid neoplasms characterized

by dysplastic features of erythroid/myeloid/megakaryocytic

lineages, progressive bone marrow failure, a varying percentage of

blast cells, and enhanced risk to evolve into acute myeloid

leukemia. It is estimated that over 10,000 new cases of MDS are

diagnosed each year and there are minimal treatment options; other

estimates have put this number higher. In addition, the incidence

of MDS is rising for unknown reasons.

Solid Tumors

In the

United States, in 2018, it is estimated there will be approximately

1,735,350 new cases of cancer resulting in over 600,000 deaths.

Greater than 80% of these cancers will be classified as solid

tumors. The most prevalent new cases of solid tumors being breast,

lung, prostate, colorectal and bladder. (American Cancer Society,

Cancer Facts & Figures 2018)

Sarcomas

A

sarcoma is a type of cancer that develops from certain tissues,

like bone or muscle. Bone and soft tissue sarcomas are the main

types of sarcoma. Soft tissue sarcomas can develop from soft

tissues like fat, muscle, nerves, fibrous tissues, blood vessels,

or deep skin tissues. They can be found in any part of the body.

Most of them develop in the arms or legs. They can also be found in

the trunk, head and neck area, internal organs, and the area in

back of the abdominal cavity (known as the retroperitoneum).

Sarcomas are not common tumors, and most cancers are the type of

tumors called carcinomas.

The

American Cancer Society's estimates for soft tissue sarcomas in the

United States for 2018 are (these statistics include both adults

and children): about 13,040 new soft tissue sarcomas will be

diagnosed (7,370 cases in males and 5,670 cases in females). 5,150

Americans (2,770 males and 2,380 females) are expected to die of

soft tissue sarcomas. The most common types of sarcoma in adults

are undifferentiated pleomorphic sarcoma (previously called

malignant fibrous histiocytoma), liposarcoma, and leiomyosarcoma.

Certain types occur more often in certain areas of the body than

others. For example, leiomyosarcomas are the most common abdominal

sarcoma, while liposarcomas and undifferentiated pleomorphic

sarcoma are most common in legs. But pathologists (doctors who

specialize in diagnosing cancers by how they look under the

microscope), may not always agree on the exact type of sarcoma.

Sarcomas of uncertain type are very common. (American Cancer

Society, Cancer Facts & Figures 2018)

CNS Markets

Chronic Neuropathic Pain

Neuropathic

pain has many causes, including trigeminal neuralgia, diabetes,

certain forms of chemotherapy, trauma, toxins, infection such as

postherpetic infection, immune deficiencies, ischemic disorders,

and multiple sclerosis. According to the latest market report

published by Persistence Market Research (November 2016) titled

“Global Market Study on Neuropathic Pain:

Anticonvulsants Drug Class Segment Projected to Witness the Highest

Growth Through 2024,”

the global neuropathic pain market was valued

at $5.2 billion in 2015 and was estimated to

reach a market valuation of $5.4 billion by 2016. The market is projected

to expand at a compound annual growth rate of 5.6% during an

eight-year forecast period 2016–2024 and

reach $8.3 billion by the end of

2024.

The chronic pain market continues to represent a major unmet

medical need. Current drugs provide a useful degree of pain relief

in only about half the patients (Nightingale, 2012). It is

estimated that only one in four patients with neuropathic pain

experiences over 50% pain relief, and 30% of patients have no or

very little relief. Very few patients achieve complete pain relief.

In most patients, pain relief is obtained at the price of

burdensome side effects. For many drugs, inadequate pain relief is

due to side effects that occur when drugs reach peak concentrations

in the blood, these side effects are dose-dependent and

dose-limiting and prevent the use of fully effective doses. As a

consequence, patients are chronically under-dosed. This is

particularly true for carbamazepine, a drug with which it may be

possible to achieve nearly complete relief of pain in many patients

who suffer from forms of neuropathic pain that respond to

carbamazepine.

Current

treatments for neuropathic pain treat the symptom (pain) and

include narcotic analgesics, voltage-gated sodium channel blockers,

voltage-gated calcium channel blockers, glutamate NMDA NR2B

antagonists (ketamine), drugs that increase monoamine transmission,

and cannabinoids. However, these therapies have safety and

tolerability issues including, for some, tolerance, abuse and

addiction liability. Many have dose-limiting side effects that

prevent patients from receiving fully effective doses of

medication, further limiting efficacy. Some of the key players operating in the global

neuropathic pain market are Depomed Inc. (NASDAQ:DEPO), Pfizer Inc.

(NYSE:PFE), Johnson & Johnson (NYSE:JNJ), Bristol-Myers Squibb

(NYSE:BMY), Eli Lilly and Company (NYSE:LLY), GlaxoSmithKline PLC

(NYSE:GSK), Sanofi S.A. (NYSE:SNY), Biogen Idec Inc. (NASDAQ:BIIB),

and Baxter Healthcare Corporation (NYSE:BAX), among

others.

Myasthenia Gravis

MG is a

rare, chronic autoimmune disease of the neuromuscular junction

caused by antibodies that attack components of the postsynaptic

membrane, impair neuromuscular transmission, and lead to varying

degrees of weakness and fatigue of skeletal muscle. Recently,

anti-cancer treatments with check-point inhibitors have been

associated in some patients with rapidly progressive severe

myasthenia gravis. The prevalence of MG in the United States is

estimated at 14 to 20 per 100,000 population, approximately 36,000

to 60,000 cases in the US (Howard, 2015). Rarely, children may show signs of congenital

myasthenia or congenital myasthenic syndrome (CMS). These are not

autoimmune disorders, but are caused by defective genes that

produce abnormal proteins instead of those that normally are

involved in cholinergic transmission: acetylcholinesterase (the

enzyme that breaks down acetylcholine), acetylcholine receptors,

and other proteins present along the muscle membrane (Engel,

2012).In some rare cases, a myasthenic syndrome is due to

bi-allelic variants in the gene encoding the vesicular

acetylcholine transporter (VAChT) located in the presynaptic

terminal (O’Grady et al, 2016). In other cases, degeneration

of the nerves that innervate muscles such as occurs with aging

(Lexel, 1997) leads to a myasthenic syndrome.

Only

two drugs are currently approved for the muscular symptoms of

myasthenia gravis, namely Mestinon® and

Prostigmine®. Both have the

same mechanism of action, and both are associated with

gastrointestinal side effects, which are an important source of discomfort for the

patient, may be the source of non-compliance, or may result in the

need to decrease the dose of ChEI to mitigate these side effects

when these become dose-limiting. In many patients the side effects

are dose limiting and prevent the administration of the fully

effective dose. Attempts at overcoming these side effects using

dose fractionation or a slow release formulation (Mestinon

TimeSpan) have been disappointing.

Motion Sickness

The current transdermal market leader for the prevention of motion

sickness is the 72-hour scopolamine patch (Gil et al., 2012)

commercialized by Sandoz. However, this medication can cause a

number of worrisome side effects., especially in the elderly, such

as confusion and memory impairment. The scopolamine patch is not

approved for children.

Manufacturing

We do not currently own or operate manufacturing facilities for the

production of clinical or commercial quantities of any of our

product candidates. We rely on a small number of third-party

manufacturers to produce our compounds and expect to continue to do

so to meet the preclinical and clinical requirements of our

potential product candidates as well as for all of our commercial

needs. We do not have long-term agreements with any of these third

parties. We require in our manufacturing and processing agreements

that all third-party contract manufacturers and processors produce

active pharmaceutical ingredients, or API, and finished products in

accordance with the FDA’s current Good Manufacturing

Practices, or cGMP, and all other applicable laws and regulations.

We maintain confidentiality agreements with potential and existing

manufacturers in order to protect our proprietary rights related to

our drug candidates.

Patents and Trademarks

University of Minnesota License Agreement

We

(through our wholly owned subsidiary Oxis Biotech, Inc.) are party

to an exclusive worldwide license agreement with the Regents of the

University of Minnesota, to further develop and commercialize

cancer therapies using TriKE technology developed by researchers at

the university to target NK cells to cancer. Under the terms of the

agreement, we receive exclusive rights to conduct research and to

develop, make, use, sell, and import TriKE technology worldwide for

the treatment of any disease, state or condition in humans. We

shall be responsible for obtaining all permits, licenses,

authorizations, registrations and regulatory approvals required or

granted by any governmental authority anywhere in the world that is

responsible for the regulation of products such as the TriKE

technology, including without limitation the FDA in the United

States and the European Agency for the Evaluation of Medicinal

Products in the European Union. Under the agreement, the University

of Minnesota will receive an upfront license fee, royalty fees

ranging from 4% to 6%, minimum annual royalty payments of $250,000

beginning in 2022, $2,000,000 in 2025, and $5,000,000 in 2027 and

certain milestone payments totaling $3,100,000.

The

following is a list of the patent applications that we licensed

from the University of Minnesota:

|

Appl. No.

|

Title

|

Country

|

Status

|

|

U.S.

Patent Application Number 62/237,835

|

Therapeutic

compounds and its uses

|

US

|

Expired

|

|

PCT

Patent Application Number PCT/US2016/055722

|

Therapeutic

compounds and methods

|

US

|

Pending

|

Daniel A. Vallera, Ph.D. License Agreement

We are

party to an exclusive worldwide license agreement with Daniel A.

Vallera, Ph.D. and his co-inventor Jeffrey Lion, or jointly, Dr.

Vallera, to further develop and commercialize DT2219ARL

(OXS1550), a novel therapy for the treatment of various human

cancers. Under the terms of the agreement, we receive exclusive

rights to conduct research and to develop, make, use, sell, and

import DT2219ARL worldwide for the treatment of any disease, state

or condition in humans. We shall be responsible for obtaining all

permits, licenses, authorizations, registrations and regulatory

approvals required or granted by any governmental authority

anywhere in the world that is responsible for the regulation of

products such as DT2219ARL, including without limitation the FDA in

the United States and the European Agency for the Evaluation of

Medicinal Products in the European Union. Under the agreement, Dr.

Vallera will receive an upfront license fee, royalty fees ranging

from 3% for net sales and 25% of net sublicensing revenues, and

certain milestone payments totaling $1,500,000.

The

following is a list of the patent applications and patents that we

licensed from Dr. Vallera under our license

agreements:

|

Pat./Pub. No.

|

Title

|

Country

|

Status

|

|

U.S.

Patent Application Number 61/160,530

|

Methods

and compositions for bi-specific targeting of

cd19/cd22

|

US

|

Expired

|

|

U.S.

Patent Number 9,371,386

|

Methods

and compositions for bi-specific targeting of

cd19/cd22

|

US

|

Issued

|

|

U.S.

Patent Application Number 15/187,579

|

Methods

and compositions for bi-specific targeting of

cd19/cd22

|

US

|

Pending

|

ID4 License Agreement

Pursuant

to a patent license agreement with ID4, dated December 31, 2014, or

the ID4 License Agreement, we received an exclusive, worldwide

license to certain intellectual property, including intellectual

property related to treating a p62mediated disease (e.g.,

multiple myeloma). The terms of this license require us to pay ID4

royalties equal to 3% of net sales of products and 25% royalty of

net sublicensing revenues. The license will expire upon expiration

of the last patent contained in the licensed patent rights, unless

terminated earlier. We may terminate the licensing agreement with

ID4 by providing ID4 with a 30 days written notice.

We will

owe the following cash amounts to ID4 Pharma upon the attainment of

the following milestones:

(i)

Filing of an

investigational new drug application with a competent regulatory

authority anywhere in the world $50,000.

(ii)

Initiation of Phase

I Human Clinical Trial: $50,000.

(iii)

Initiation of Phase

II Human Clinical Trial: $100,000.

(iv)

Initiation of

pivotal Phase III Human Clinical Trial: $250,000. and

(v)

Receipt of the

first marketing approval: $250,000

The

following is a list of the patent applications and patent that we

licensed from ID4 under the ID4 license agreement:

|

Pat./Appl. No.

|

Title

|

Country

|

Status

|

|

U.S.

Patent Number

9,580,382

|

P62zz

chemical inhibitor

|

US

|

Issued

|

|

U.S.

Patent Application Number 61/521,287

|

P62zz

chemical inhibitor

|

US

|

Expired

|

|

PCT

Patent Application Number PCT/US2012/049911

|

P62zz

chemical inhibitor

|

PCT

|

Expired

|

|

U.S.

Patent Application Number 14/727,710

|

P62zz

chemical inhibitor

|

US

|

Pending

|

|

Chinese

Patent Application 201280048718

|

P62zz

chemical inhibitor

|

US

|

Pending

|

Patents for AccuBreak Tablets

We have

in-licensed the rights to use the AccuBreak patents with drugs

that, like carbamazepine, are voltage-gated sodium channel blockers

in North America. The license field includes voltage gated sodium

channels inhibitors and blockers for the treatment of epilepsy,

neuropathic pain, and bipolar disorder.

Under

the agreement, AccuBreak received an upfront license fee of

$35,000, royalty fees ranging from 2.5% to 5%, minimum annual

royalty payments, and 20% of net sublicensing

revenues.

We will

owe the following cash amounts to AccuBreak upon the attainment of

the following milestones:

●

$50,000 six months

after the first approval of the first indication by the

FDA;

●

$50,000 nine months

after the first approval of the first indication by the

FDA;

●

$100,000 12 months

after the first approval of the first indication by the

FDA;

●

$25,000 upon